TL;DR

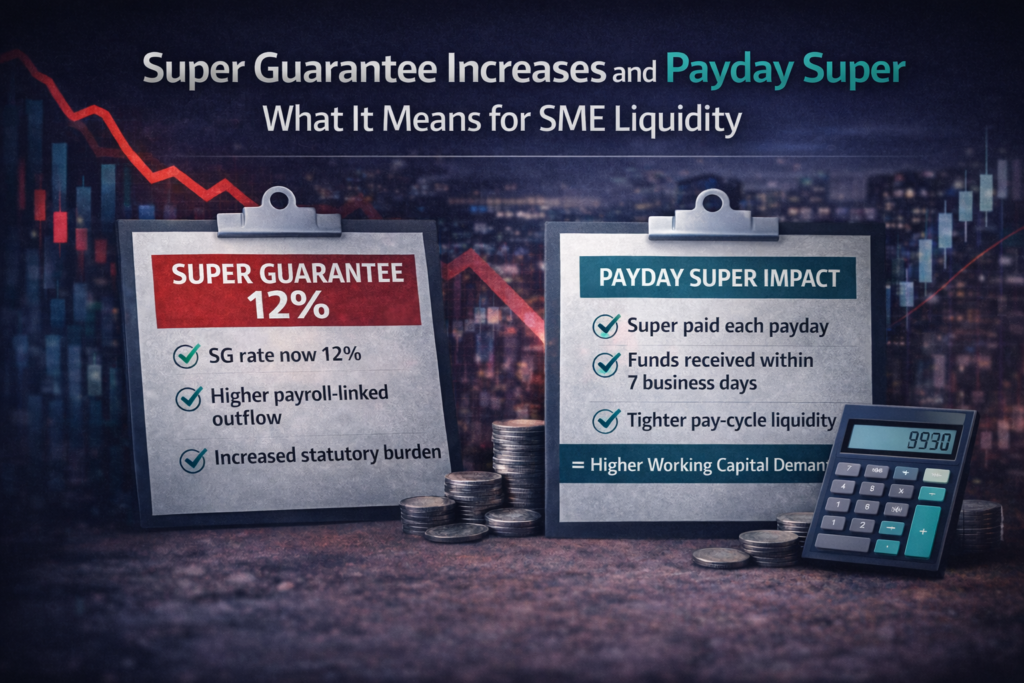

- The Super Guarantee (SG) rate increased to 12% from 1 July 2025 and is scheduled to remain at 12%. (ATO SG rates)

- From 1 July 2026, Payday Super requires employers to pay SG at the same time as wages, and in most cases it must be received by the employee’s super fund within 7 business days. (ATO Payday Super)

- These changes tighten cashflow timing for employer SMEs, especially those with 30–60 day customer terms.

- The key risk is a working capital timing mismatch: payroll and super go out now; receipts arrive later.

- Use the Payday Super Calculator to quantify the pay-cycle impact and plan prevention early.

Run the Payday Super Calculator

Definition: What Is the Super Guarantee (SG)?

The Super Guarantee (SG) is the compulsory percentage of an eligible employee’s earnings that employers must contribute to the employee’s super fund. The SG rate increased to 12% from 1 July 2025. (ATO Small Business Newsroom)

Definition: What Is Payday Super?

Payday Super is a regulatory change starting 1 July 2026 that requires employers to pay SG at the same time as wages. In most cases, the super contribution must be received by the employee’s super fund within 7 business days after payday (with limited exceptions). (ATO Payday Super)

Practical meaning: super becomes a pay-cycle cashflow event, not a quarterly “admin deadline.”

Why This Is a Liquidity Story (Not Just a Compliance Story)

For employer SMEs, super changes affect liquidity because payroll obligations have fixed timing. Most SMEs cannot “move payroll.”

Many SMEs also sell on terms:

- Invoices paid in 14–60 days

- Receipts arrive unevenly

- Payroll and statutory outflows occur on schedule

When outflows occur earlier or more frequently than inflows, cashflow strain increases even if revenue is rising.

The Two-Part Impact on SME Cashflow

- Higher baseline cost (SG at 12%): every pay run has a larger super component than prior years. (ATO SG rates)

- Tighter timing (Payday Super from 1 July 2026): super must be paid alongside wages and generally received within 7 business days, reducing timing buffer for employer cash management. (ATO Payday Super)

Together, these changes can increase the need for structured working capital in payroll-heavy businesses.

Real Example Numbers: What 12% SG Looks Like in Cash Terms

Example: 15 employees, weekly payroll, B2B customer terms.

- Weekly gross wages: $30,000

- SG rate: 12%

- Weekly SG liability: $30,000 × 12% = $3,600

- Monthly SG (approx.): $3,600 × 4.33 = $15,588

- Average customer payment timing: 35–45 days

Under Payday Super from 1 July 2026, this becomes a pay-cycle cash requirement aligned to wages. If customer receipts arrive 35–45 days later, the business is bridging multiple pay cycles of wages plus super before cash is collected.

This is the structural issue: revenue can grow while liquidity tightens.

Which SMEs Are Most Exposed?

- Payroll-heavy industries: hospitality, construction, healthcare, labour-hire, retail, transport

- Any business selling on terms: 30–60 day invoices, progress claims, milestone billing

- Growth-stage employers: headcount rising faster than cash reserves

- Thin-margin operators: where small timing changes create large stress

Media Angle: Why This Is Newsworthy

- SG is now at 12% from 1 July 2025, increasing baseline employer outflows. (ATO)

- Payday Super starts 1 July 2026, shifting super into the pay-cycle, tightening SME cashflow timing. (ATO)

- For SMEs already experiencing payroll pressure, the change increases the importance of forecasting and working capital structure.

If you’re a journalist or editor covering small business finance: this is a policy change with direct cashflow consequences for employer businesses.

Prevention: The Fastest Way to Quantify Your Exposure

Most SMEs do not model super as a pay-cycle cashflow requirement. Do the stress test now, before 1 July 2026 forces operational changes.

Use the Payday Super Calculator

Use it to estimate the pay-cycle cash impact and whether your current cash buffer or facility structure can absorb it.

FAQ: Super Guarantee, Payday Super, and SME Liquidity

What is the Super Guarantee rate now?

The SG rate is 12% from 1 July 2025. (ATO SG rates)

When does Payday Super start?

Payday Super starts from 1 July 2026. Employers must pay super at the same time as wages and, in most cases, ensure it is received by the super fund within 7 business days after payday. (ATO Payday Super)

Why does this matter for cashflow?

Because payroll and super are fixed-timing outflows, while customer receipts often arrive later. The timing gap must be funded by cash reserves, faster collections, or working capital facilities.

Which businesses should stress-test first?

Employer SMEs with weekly/fortnightly payroll, growing headcount, and customers on 30–60 day terms should stress-test early.

What is the fastest way to model the impact?

Use the Payday Super Calculator to quantify the pay-cycle cash effect and identify whether prevention steps are required.

For Accountants, Bookkeepers, and Advisors

These regulatory changes create a predictable advisory trigger: employer clients who were “fine” under older payment habits may face pay-cycle liquidity compression under Payday Super timing.

GPS Finance Group works with referral partners to:

- Use the Payday Super Calculator as a prevention tool

- Identify employer clients exposed to pay-cycle cash troughs

- Structure revolving working capital aligned to payroll timing

- Reduce recurring statutory stress cycles

Apply to Become a GPS Finance Referral Partner

Next Step

Run the Payday Super Calculator

Advisors: Join the GPS Finance Referral Program