TL;DR

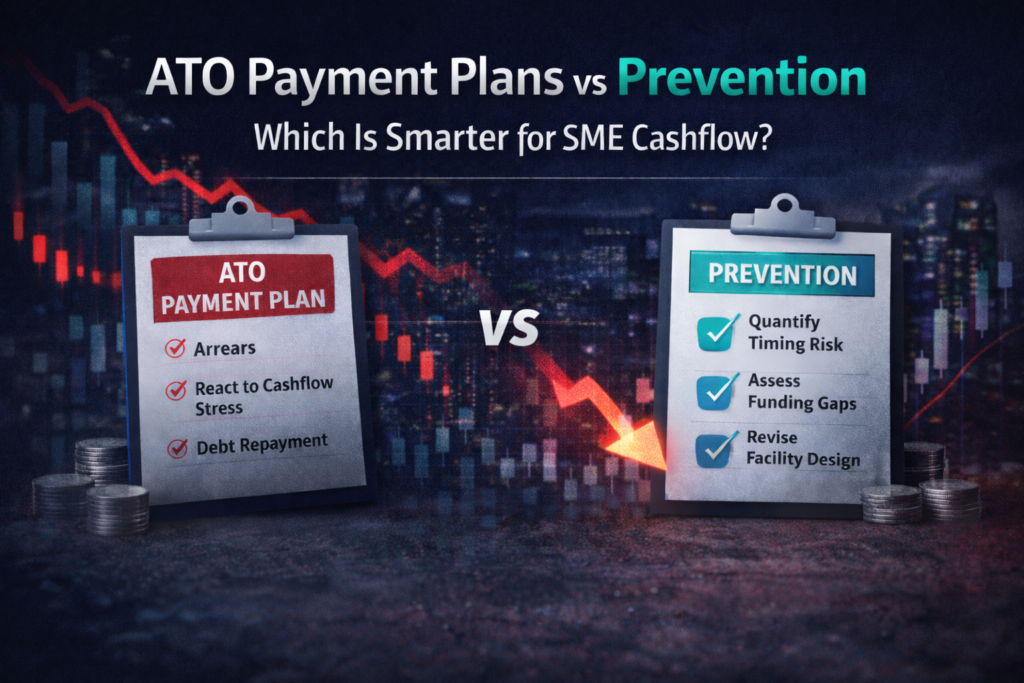

- An ATO payment plan can provide short-term relief, but it is usually a response to arrears after cashflow stress has already arrived.

- Prevention is a cashflow design strategy: tighter forecasting, earlier detection of liquidity compression, and appropriate working capital structure.

- From 1 July 2026, Payday Super increases the frequency of super cash outflows, which can amplify timing pressure for employer businesses.

- The fastest prevention step is to quantify timing risk using the Payday Super Calculator before arrears begin.

- Advisors can use this as a trigger to protect clients and strengthen relationships through proactive working capital planning.

Run the Payday Super Calculator

Definition: What Is an ATO Payment Plan?

An ATO payment plan is an arrangement that allows a business to repay a tax debt to the Australian Taxation Office over time, rather than paying the full amount immediately. It is typically used when a business cannot meet an upcoming or overdue obligation in full.

It can be useful for stabilisation. It is not a structural fix.

Definition: What Does “Prevention” Mean in Cashflow Terms?

Prevention means identifying cashflow timing pressure early and correcting the underlying cause before tax arrears occur. In practice, prevention is:

- Measuring payroll-linked obligations (including super) as a pay-cycle cashflow event

- Stress-testing whether receivables timing supports payroll timing

- Structuring working capital facilities to match operating cycles

- Creating liquidity buffers before obligations become late

The Core Issue: ATO Plans Treat Symptoms, Not Structure

Most SMEs do not “suddenly become non-compliant.” They experience cashflow timing mismatch where outflows occur earlier or more frequently than inflows.

Common drivers include:

- Payroll growth while customers remain on 30–60 day terms

- Seasonal or lumpy revenue

- Quarter-end stacking of obligations

- From 1 July 2026: more frequent super payment timing under Payday Super for employer businesses

An ATO payment plan may stop immediate escalation. But if the timing mismatch remains, the business often cycles back into stress.

When an ATO Payment Plan Can Be the Right Move

An ATO payment plan can be rational when:

- You have a one-off disruption (lost contract, unexpected expense, temporary debtor issue)

- Your underlying margins and cashflow model are stable, and you need time

- You have a clear path to repayment that does not rely on optimism

In these cases, a payment plan is stabilisation, not a long-term operating model.

When an ATO Payment Plan Is a Warning Signal

An ATO plan is a warning signal when:

- It is being used repeatedly (or for multiple obligation types)

- Payroll has grown but working capital facilities have not been updated

- Super obligations cause recurring pay-cycle pressure

- Directors are injecting personal funds to bridge routine obligations

- You are relying on late customer payments to fund statutory obligations

These are structure problems. Not motivation problems.

Payday Super from 1 July 2026: Why Prevention Matters More

From 1 July 2026, employers must pay super at the same time as wages, generally ensuring it is received by the employee’s super fund within a short timeframe. This shifts super from being treated as a periodic task to a pay-cycle cashflow requirement.

For many employer businesses, this increases the need for prevention because:

- Cash leaves the business more frequently

- The buffer some businesses relied on disappears

- Payroll-driven liquidity compression becomes visible sooner

If your customer payment terms do not change, the working capital gap can widen.

Prevention in Practice: The Fastest 3-Step Method

- Quantify the timing risk: model payroll and super as a recurring cashflow event.

- Compare inflows vs outflows: align customer payment timing to payroll timing reality.

- Correct the structure: ensure working capital facilities match operating cycles.

Start with the simplest step: quantify the risk.

Use the Payday Super Calculator

Consultation: Discuss Prevention and Facility Structure

If the calculator indicates potential cashflow compression, the next step is to review the structure of your working capital and cashflow cycle.

This is designed to identify whether an ATO plan is a short-term stabiliser or whether prevention via facility structure is the smarter move.

FAQ: ATO Payment Plans vs Prevention

Is an ATO payment plan bad?

No. It can be a rational short-term stabilisation tool. The risk is when it becomes the default solution to an underlying timing mismatch.

What is the difference between a payment plan and prevention?

A payment plan repays existing debt. Prevention redesigns cashflow timing and funding structure so arrears are less likely to occur.

How does Payday Super change the equation?

From 1 July 2026, super becomes a pay-cycle cashflow event for employers. This can tighten liquidity if customer receipts lag payroll outflows.

What is the fastest prevention step?

Quantify exposure with the Payday Super Calculator, then review working capital structure.

When should I book a consultation?

If you are considering an ATO payment plan, or if you regularly feel pay-cycle pressure around payroll and super, a structured review can identify whether prevention is smarter than repeatedly reacting.

For Accountants, Bookkeepers, and Advisors

This topic is a predictable advisory trigger. Employer clients under Payday Super timing pressure may drift toward ATO plans unless someone redesigns the liquidity structure.

GPS Finance Group works with referral partners to:

- Use the Payday Super Calculator as a prevention tool

- Identify clients most exposed to pay-cycle liquidity compression

- Structure revolving working capital facilities aligned to payroll cycles

- Reduce recurring ATO stress cycles and protect client relationships

Apply to Become a GPS Finance Referral Partner

Next Step

Run the Payday Super Calculator

Advisors: Join the GPS Finance Referral Program