TL;DR

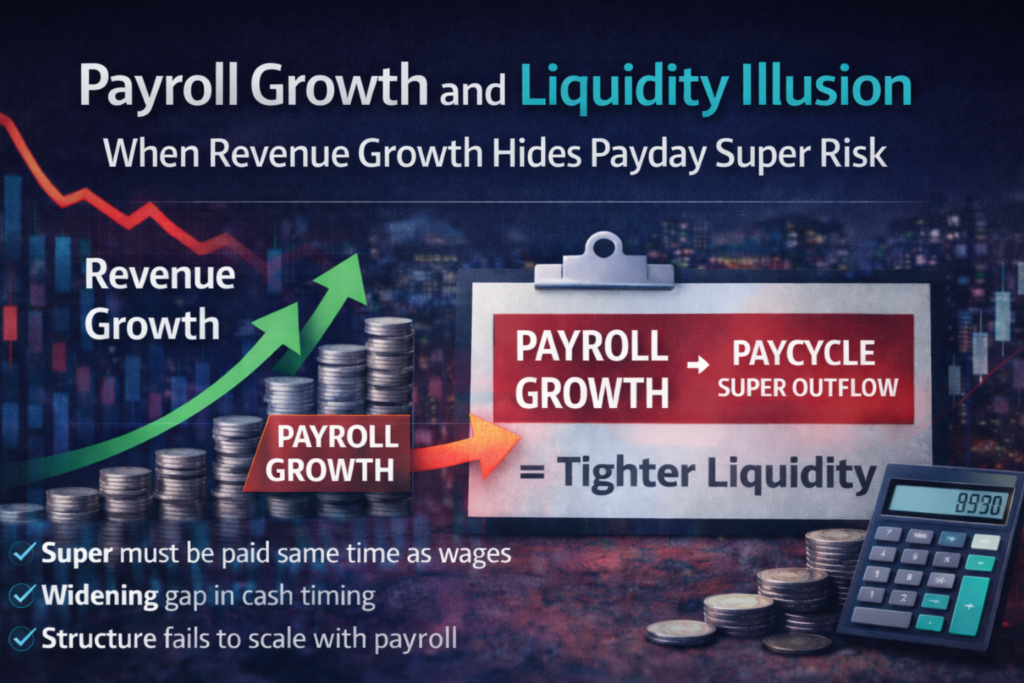

- Revenue growth can make an SME look healthier while liquidity quietly tightens.

- Payroll is a fixed-timing outflow; customer receipts often arrive later.

- From 1 July 2026, Payday Super requires super to be paid at the same time as wages, generally received by the fund within 7 business days, making super a pay-cycle cashflow event.

- As headcount and wages rise, super outflows rise automatically, even if profit margins hold.

- Use the Payday Super Calculator to quantify the cash timing impact and prevent pay-cycle squeeze.

Run the Payday Super Calculator

Definition: What Is the “Liquidity Illusion”?

The liquidity illusion is when a business appears strong because revenue and profit are rising, but available cash is falling due to timing mismatch between inflows and outflows.

It is common in growing SMEs because:

- sales growth does not guarantee fast collections

- expenses like payroll move immediately with growth

- statutory obligations scale automatically with wages

Definition: What Is Payday Super Timing Risk?

Payday Super timing risk is the liquidity pressure created when superannuation becomes a pay-cycle cashflow requirement rather than a periodic payment habit.

From 1 July 2026, employers must pay super at the same time as wages, generally ensuring it is received by the employee’s super fund within 7 business days (with limited exceptions). Official ATO overview:

Why Revenue Growth Masks Super Liability Risk

Revenue growth changes optics. Payroll growth changes reality.

What often happens in growth:

- New contracts increase sales, but payment terms stay at 30–60 days.

- Headcount increases immediately to deliver the work.

- Payroll rises on a fixed cycle (weekly/fortnightly).

- Super rises with payroll, and from 1 July 2026 becomes a pay-cycle cash outflow.

This is how “more revenue” can produce “less cash.”

The Timing Mismatch: A Simple Model

Most SMEs are structurally exposed when:

- Receivables timing: customers pay in 30–60 days

- Payroll timing: wages are paid weekly/fortnightly

- Super timing (from 1 July 2026): super is paid at the same time as wages

The gap between paying employees and being paid by customers must be funded by:

- cash reserves

- faster collections

- customer deposits / milestone billing

- revolving working capital facilities

Real Example Numbers: Growth That Looks “Good” but Tightens Cash

Scenario: An SME grows revenue by adding staff to service demand.

- Before growth: 8 employees, fortnightly wages $28,000

- After growth: 14 employees, fortnightly wages $52,000

- Customer payment terms: average 45 days

- Super rate (illustrative): 11.5%

Super cash impact per pay cycle:

- Before growth: $28,000 × 11.5% = $3,220 per fortnight

- After growth: $52,000 × 11.5% = $5,980 per fortnight

- Increase: $2,760 more in super cash outflow each fortnight

Monthly effect (approx.):

- After growth: $5,980 × 2 = $11,960 of super-linked cash outflow per month

If customers pay in 45 days, the business is funding payroll and super for roughly 1.5 months before receipts land. Growth increases the bridge requirement. Nothing “went wrong.” The structure simply did not scale with payroll timing.

Common Signs You’re Living the Liquidity Illusion

- Revenue is up, but cash at bank is not improving.

- Debtors are rising faster than sales.

- You rely on short-term credit to cover recurring payruns.

- Quarterly reporting looks fine, but pay-cycle cash troughs are deeper.

- Directors inject funds to “smooth” payroll or statutory payments.

Prevention: How to Remove the Illusion

The fix is not “try harder.” The fix is to measure and structure the timing gap.

- Measure: forecast cash at pay-cycle level, not monthly averages.

- Stress-test: model super as a pay-cycle outflow aligned to wages.

- Correct: align working capital facilities to payroll and receivables timing.

Stress-Test Your Payday Super Exposure

The fastest step is to quantify the pay-cycle impact under the new timing rules.

Use the Payday Super Calculator

Use it to identify whether your growth is increasing your cash bridge requirement and whether your facility structure matches your operating cycle.

FAQ: Payroll Growth, Liquidity, and Payday Super

How can revenue grow but cash get worse?

Because payroll and supplier payments often accelerate immediately, while customer receipts lag. The timing gap widens as the business scales.

Why does payroll growth increase super risk?

Super scales automatically with wages. From 1 July 2026, super becomes a pay-cycle cash outflow aligned to wages, tightening liquidity timing.

What is the biggest forecasting mistake SMEs make?

Using monthly averages instead of pay-cycle timing. Payroll happens weekly/fortnightly; collections are uneven. Averages hide the trough.

What is the fastest way to quantify the impact?

Use the Payday Super Calculator to model payroll-linked super outflows and assess the working capital buffer required.

What should I do if the model shows a pay-cycle squeeze?

Review collections discipline, billing cadence, and whether a revolving working capital facility is needed to align cash inflows with payroll outflows.

For Accountants, Bookkeepers, and Advisors

Payroll growth plus Payday Super timing is a predictable trigger for liquidity compression. The advisor who stress-tests timing early can prevent arrears and reduce crisis cycles for employer clients.

GPS Finance Group works with referral partners to:

- Use the Payday Super Calculator to surface timing risk

- Identify employer clients exposed to pay-cycle liquidity compression

- Structure revolving working capital aligned to payroll cycles

- Reduce recurring ATO stress cycles and protect client relationships

Apply to Become a GPS Finance Referral Partner

Next Step

Run the Payday Super Calculator

Advisors: Join the GPS Finance Referral Program